")

Robert Way

Instacart (NASDAQ:CART) has struggled in the wake of the pandemic, with a reversion in consumer buyer behavior weighing on growth and margins. The company’s growth now appears to be picking up again though, and its cash flows are trending higher. While this is positive, Instacart’s customer acquisition costs are also rising, which could be due to either rising competition or difficulty attracting new customers to the segment.

Despite Instacart’s dominance in the grocery vertical, competition is likely to increase in coming years, both from grocers and from companies leveraging their delivery networks to target a range of verticals. Instacart is tightly integrating its business with grocers, potentially creating a sizeable barrier to entry. There is a tension inherent in this strategy, though, as Instacart’s business takes control of the customer relationship from grocers. As a result, I think it is likely that larger grocers will want to direct ecommerce through their own websites/apps longer term.

The high costs associated with manual picking also mean there is a large incentive to automate as much of this process as possible. Automation could undermine the dynamics of Instacart’s platform and make the company more vulnerable to both grocers and the likes of DoorDash (DASH).

Market

Groceries are a $1.1 trillion industry in the US, presenting companies like Instacart with a large opportunity. Americans shop for groceries 1.6 times per week on average, spending $438 per month. Even with Instacart’s 12-year history and the boost provided by the pandemic, online grocery penetration is still only something like 12% though. It is also a reasonably concentrated industry, with the top 20 grocers constituting 68% of the market.

Instacart’s business is built around the convenience that ecommerce offers consumers and the potential incremental source of revenue that it offers grocers. It is worth noting that long-term, this type of service is unlikely to meaningfully impact industry sales but could be a meaningful headwind to grocer margins.

Logistics is at the heart of Instacart’s business and relative to other delivery categories, groceries present some unique challenges:

- Diversity – the average grocer carries over 31,000 products across a wide range of categories.

- Perishables – perishables account for 16% of North American grocery sales.

- Low Margins and High Fixed Costs – typical grocery retail margins are around 6%, making grocers sensitive to small changes in performance.

In some ways, groceries are a relatively attractive delivery category though. Orders tend to be relatively large and are often less time sensitive, allowing deliveries to be scheduled ahead of time and batched together.

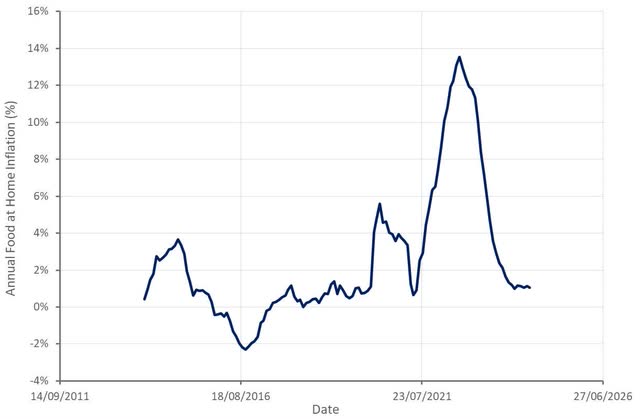

While groceries are a necessity, delivery is more of a luxury, which probably means that Instacart’s business will prove sensitive to the economic cycle. Employment dictates the ability and value (amount of free time) of grocery delivery, meaning a significant drop in employment is likely to impact demand for Instacart’s service. The moderation of food inflation could provide a modest tailwind, though, assuming it meaningfully eases pressure on consumer wallets.

Figure 1: Food at Home Inflation in the US (source: Created by author using data from The Federal Reserve)

While its marketplace is currently performing well, soft macroeconomic conditions are impacting Instacart through its advertising business. Some large CPG brands are struggling and pulling back on advertising as a result. Instacart’s ad performance and targeting and attribution capabilities are helping to insulate it from industry headwinds though. Emerging brands are also helping to support growth in the face of weak ad spend by large organizations.

Instacart faces competition from a range of companies, including Amazon (AMZN) and Thrive Market. Brick and mortar retailers like Target (TGT) and Walmart (WMT) are also expanding their digital presence, although some companies in this category have chosen to partner with Instacart. Delivery companies like DoorDash and Uber (UBER) are also expanding their grocery delivery businesses.

Instacart has a dominant position in groceries, with more than a 50% share of small baskets and in excess of a 70% share of large baskets ($75+). This is important as large baskets represent 75% of industry revenue. Instacart has suggested that the competitive environment has been fairly stable.

Instacart

Instacart was founded in 2012 to enable ecommerce for grocers and provide consumers with convenience. The company manages an online platform and coordinates an independent fleet of around 600,000 shoppers who pick and deliver orders.

Instacart is the largest online grocery player in North America, with around 25 million people using the service in the past year. The company is able to reach over 95% of households in North America and has 7.7 million monthly active orders, who spend $317 per month on average.

Instacart’s membership program, Instacart+, offers unlimited free delivery on orders over a certain size, a reduced service fee, credit back on eligible pickup orders, and exclusive benefits. The program currently has around 5.1 million members.

Instacart partners with over 1,400 retail banners, which operate in excess of 80,000 stores and represent more than 85% of US grocery sales. The company estimates that it provided 5% of the sales of its top 20 retail partners in 2022, up from 0.6% in 2018.

Instacart offers a range of fulfillment options, including standard, priority, and scheduled delivery, as well as pickup. The company also now offers a free delivery option to all consumers with its Super Saver delivery windows. Attracting new customers and retailers to the platform is a key driver of delivery efficiency. Increased density allows Instacart to offer faster on-demand delivery and batch more orders together, with batching particularly important for unit economics.

Using shoppers to pick orders could prove to be an inefficient solution long-term, though, with robotics set to offer a viable alternative as capabilities increase and costs decline. As a result of the high cost of picking and delivery, Instacart’s delivery fees, tips, and markups add roughly 25% to the cost of an order, which is likely a key reason that ecommerce hasn’t achieved greater penetration of the grocery vertical.

Ocado is a leader in robotics for grocery ecommerce. Its Andover operation is capable of processing 3.5 million items or around 65,000 orders every week. Kroger (KR) is deploying Ocado robotic pickers at some of its fulfillment centers. Kroger first started installing the technology in 2021 and the relationship has expanded over time. Kroger generated $12 billion in digital sales in 2023, up 12% YoY.

Symbotic (SYM) is also seeing significant success in the warehouse automation space, but its solutions have so far been more targeted at distribution centers. The company is developing a system that can handle perishables and a breakpack system though. The breakpack system is for anything that goes into the store that isn’t full cases. Symbotic believes that this solution could become an important part of omnichannel warehouses, providing both case and handling capacity. Presumably, as Symbotic’s technology develops, it will look to address areas like ecommerce fulfillment.

Instacart has considered creating robotized fulfillment centers in the past. The company would have contracted out the automation side of things to a robotics firm though, rather than trying to develop its own solution. More recently, Instacart’s CEO has suggested that human shoppers are faster and less expensive. This is largely due to the fact that high order density is needed for automation to work, as current systems tend to be unwieldy and deployed in large facilities. Selection and delivery from a warehouse rather than a store adds to delivery time and expense, negating the benefits of automation. While technology is likely to result in more automation over time, some items are likely to prove more resistant to automation than others (e.g. fruit & vegetables). As a result, shoppers are likely to retain their importance for some time.

Instacart is also introducing AI for customer support. Its Carebot resolves customer inquiries in an average of under 3 minutes. The company is trying to reduce the percentage of inquiries that require an agent while maintaining or providing a better service.

Outside of its core grocery business, Instacart continues to add new retailers to its marketplace, like Sally Beauty and The Home Depot. This is very much in line with DoorDash’s strategy, with DoorDash expanding from food delivery into areas like groceries and beauty. Instacart has also partnered with Uber Eats to bring meal delivery to its users and has stated that it is pleased with the progress of this initiative.

There is also a large international opportunity, although Instacart is currently focused on the North American market. While this makes sense, there is likely to be a first mover advantage that could make it difficult for Instacart to build a meaningful international business later on. Caper Carts is providing Instacart with some international presence without committing significant resources though. For example, ALDI in Austria is interested in Caper Carts and Instacart’s suite of in-store products more broadly.

Caper Carts are shopping carts that feature a screen, barcode scanner and electronic payment capabilities. These carts help to improve the customer experience by unifying online and in-store shopping, and enable Instacart to provide in-store advertising. Caper Carts are designed to work with existing POS systems and loyalty programs and help to prevent shrink. There are hundreds of Caper Carts live in the market, with thousands to be launched by the end of 2024.

In addition to its marketplace, Instacart has an enterprise platform, which extends its business into physical stores. Instacart’s Enterprise Platform provides grocers with solutions that help them to manage their online and physical storefronts. This covers areas like ecommerce, fulfillment, Connected Stores, ads and marketing, and insights. These solutions are modular in nature, enabling retailers to pick solutions according to their needs. Instacart’s technology also connects shopping surfaces, allowing customers to buy from retailers online and in-store in a seamless fashion. In-store technology includes smart carts, mobile checkout and electronic shelf tags.

Instagram’s Marketplace and Enterprise Platform provides it with deep integration into retailers’ systems. This includes areas like loyalty programs, circulars, and price optimization algorithms. This is potentially Instacart’s biggest competitive advantage, as it reduces the probability of losing retailers and makes it more difficult for competitors to introduce comparable services.

Instacart is trying to create an omnichannel retail media network, and scaling its marketplace and enterprise offerings are an important part of this effort. The company already has a relatively large advertising business, which is an important driver of both growth and profitability. Instacart continues to innovate in this area, recently announcing new ad formats, like recipes, locations, and bundles, which are new ad formats. The company also plans on introducing in-store ads on Caper Carts’ screens. Instacart Ads enable CPG companies to target shoppers on Instacart and in-store. Instacart’s advertising business has over 6,000 active brand partners. This part of the business has seen significant success in recent years as Instacart has high intent customers and access to data which enables targeting and attribution. Long-term, Instacart is targeting advertising revenue equal to 4-5% of GTV.

Financial Analysis

Instacart’s GTV increased 10% YoY in the second quarter, with orders up 7% and average order value increasing 3%. Advertising and other revenue increased 11% YoY, driven by growth from emerging brands on the platform. This growth more than offset the pullback in spending from some of Instacart’s large brand partners, which are facing headwinds in their own businesses.

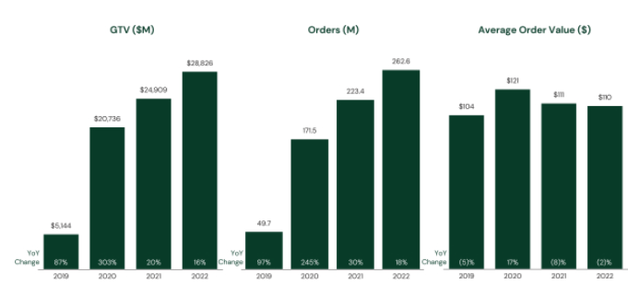

Instacart’s growth has stalled over the past few years, although it could now be reaccelerating. Instacart expects $8.1-$8.25 billion GTV in the third quarter, an increase of 8-10% YoY driven by increased order volumes. Restaurant orders are expected to provide a modest growth contribution. This guidance likely implies a modest growth acceleration in the third quarter.

Figure 2: Instacart Gross Transaction Value (source: Instacart)

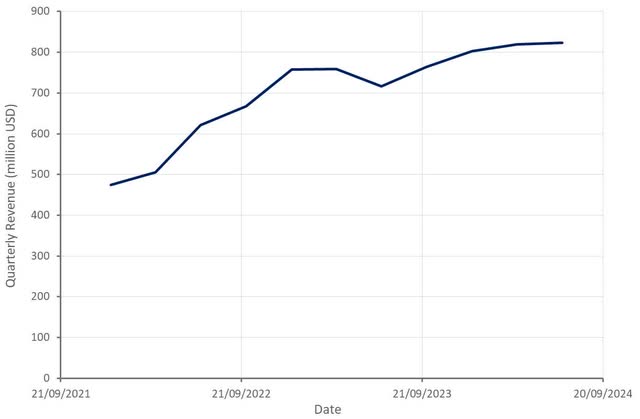

Figure 3: Instacart Revenue (source: Created by author using data from Instacart)

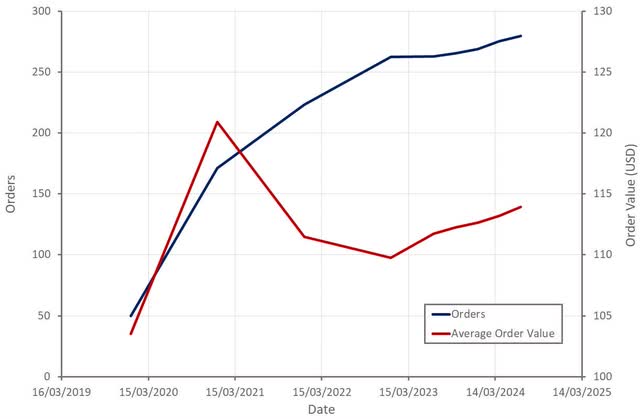

Instacart is focused on customer acquisition and is pleased with its efforts in this area. The company has 25 million annual customers, meaning there is also a large opportunity in increasing purchase frequency. These customers order 11 times a year on average, far less than typical monthly active users.

Figure 4: Instacart Orders (source: Created by author using data from Instacart)

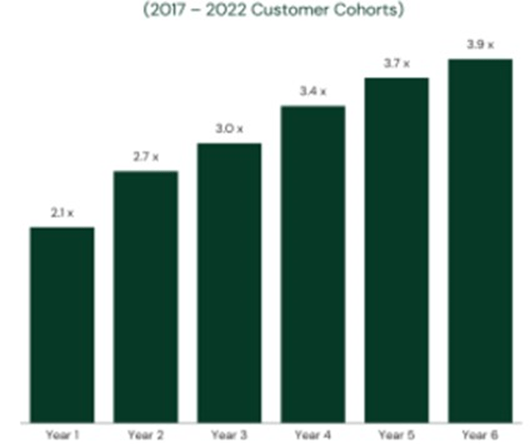

Instacart monthly active orders tend to increase their purchase frequency over time, driving continued growth of Instacart’s business from within its existing customer base.

Figure 5: Instacart Monthly Orders per Monthly Active Order (source: Instacart)

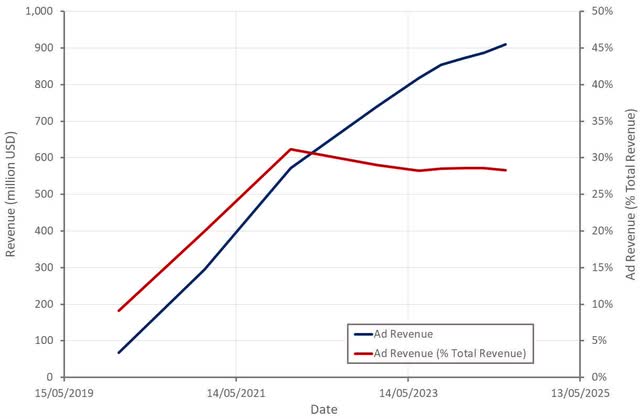

Advertising has grown to be a large part of Instacart’s business over the past five years, although progress in this area now appears to be moderating. Advertising is a high margin source of revenue and is probably one of the primary reasons that Instacart’s business has generally been profitable in recent years.

If Instacart is unable to generate a higher proportion of its revenue from advertising going forward, it may be difficult for the company to significantly improve its margins.

Advertising is also dependent on Instacart’s ability to expand, or at least maintain, its user base. This may become more difficult in coming years as grocers try to retake control of their customer relationships and competition from companies like DoorDash increases.

Figure 6: Instacart Ad Revenue (source: Created by author using data from Instacart)

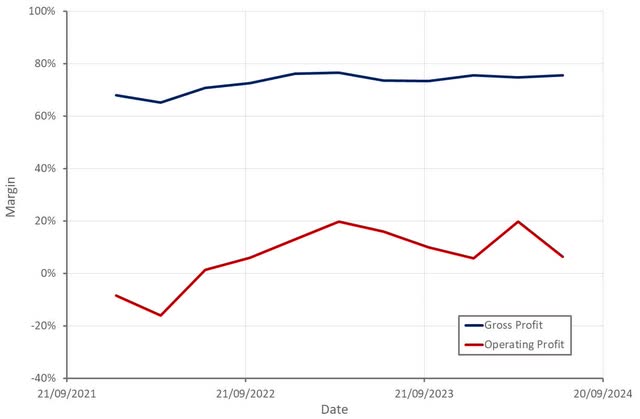

Instacart’s gross margins are quite high given the nature of its business. I would attribute this to advertising revenue and its enterprise platform as much as anything. The properties of grocery delivery should also make it more profitable than food delivery.

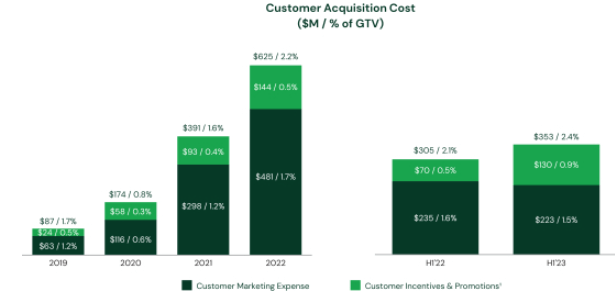

Instacart has generally been profitable and generating solid cash flows over the past few years. Customer acquisition costs have been rising in recent years though, which makes me question Instacart’s ability to continue driving margins higher. This appears to largely be the result of churn, with the company’s sales and marketing budget now predominantly going towards replacing churned customers. While the company’s retention rate has been trending higher, it is lower than many of its peers at 61% QoQ. Instacart should be able to address this somewhat through measures like subscriptions, loyalty programs and by expanding its offerings.

Stock-based compensation is expected to begin normalizing as Instacart laps its IPO quarter, which should see the company’s GAAP margins come more into line with its cash flows.

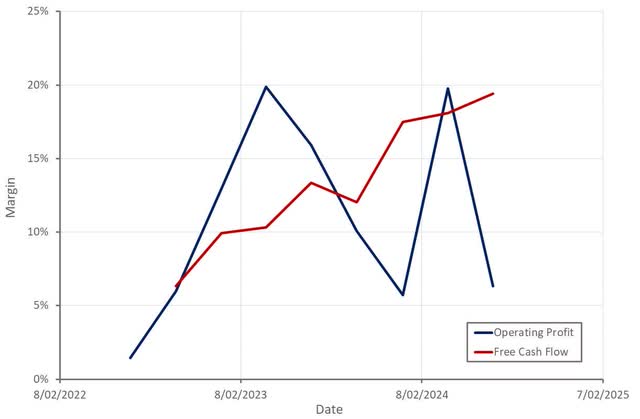

Figure 7: Instacart Margins (source: Created by author using data from Instacart)

Figure 8: Instacart Customer Acquisition Costs (source: Instacart)

Figure 9: Instacart Cash Flows (source: Created by author using data from Instacart)

Conclusion

Instacart has a relatively low revenue multiple for a growing and profitable company. As a result, it could offer investors reasonably strong returns long term. This depends on ecommerce adoption in groceries and Instacart’s ability to maintain its leadership position as competition increases, both from retailers and other delivery companies.

While I believe that Instacart’s Enterprise Platform is an important barrier to entry, the companies with the most efficient logistics are likely to be winners in the coming years. Logistics efficiency is largely a function of scale and economies of density, and Instacart’s narrow focus could be a disadvantage in this regard.

Grocers will also want to ensure they retain control of the customer relationship, particularly as retail media networks grow in importance and customer data becomes more valuable. As a result, it seems likely that larger grocers will want to drive customers through their own online storefronts. Instacart’s Enterprise Platform positions it for this eventuality, but it would still probably cap upside.

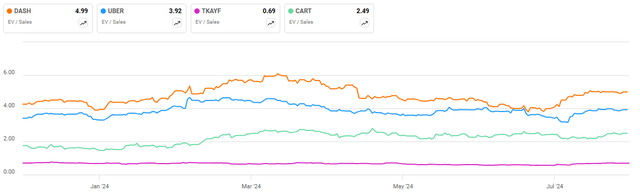

Figure 10: Instacart EV/S Ratio (source: Seeking Alpha)

link